The MBA for

Gen Z

Entrepreneurs

Every young adult has a unique talent waiting to shine. Join the Entrepreneurship Academy for the next generation of leaders.

Online

Bite-sized Lessons

Certificate

Book a call to learn more about the program.

Learn from the Experts

Faculty

Meet Your Instructors

MORE ABOUT US

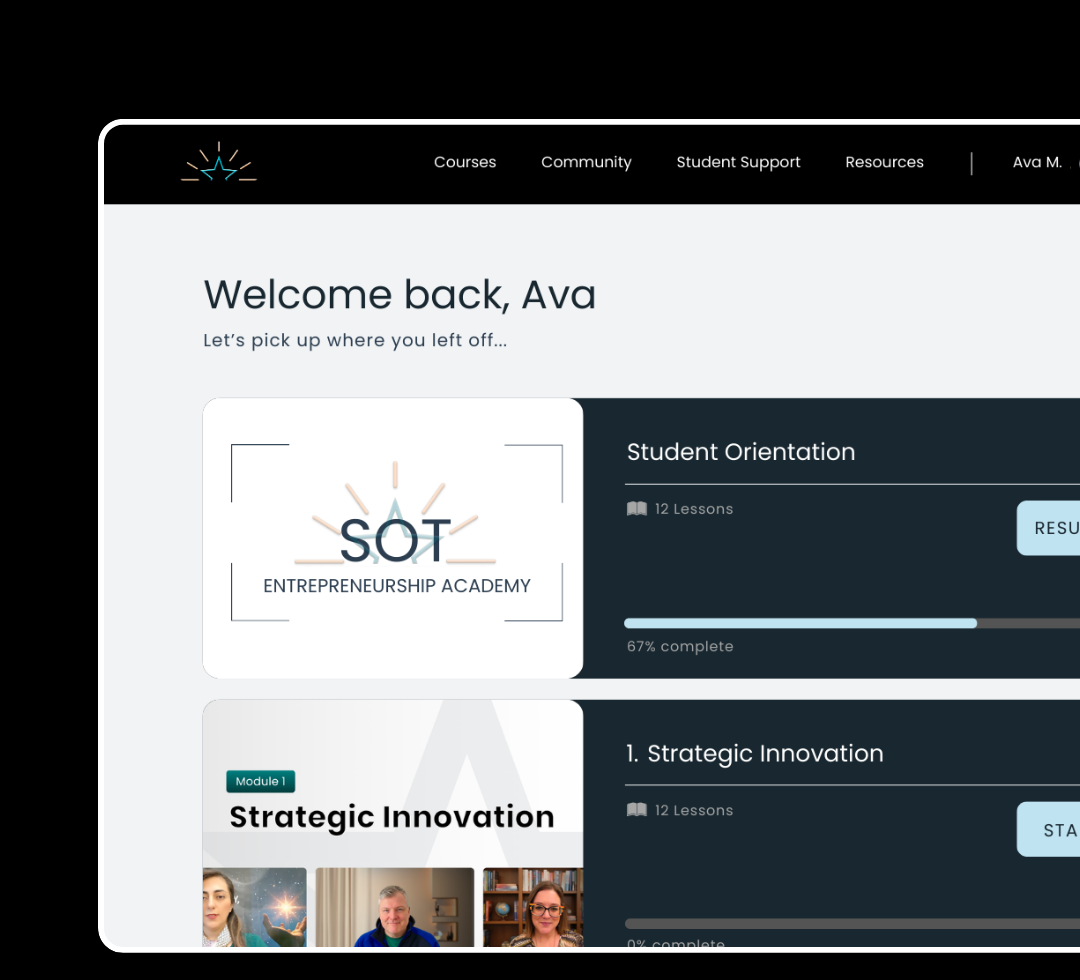

Stay Organised with

Gen Z MBA™ Program

A curated Entrepreneurship journey where ambitious ages 13–27 build real venture, command money, leadership and wield AI as advantage.

LEARN MOREWHY SOT

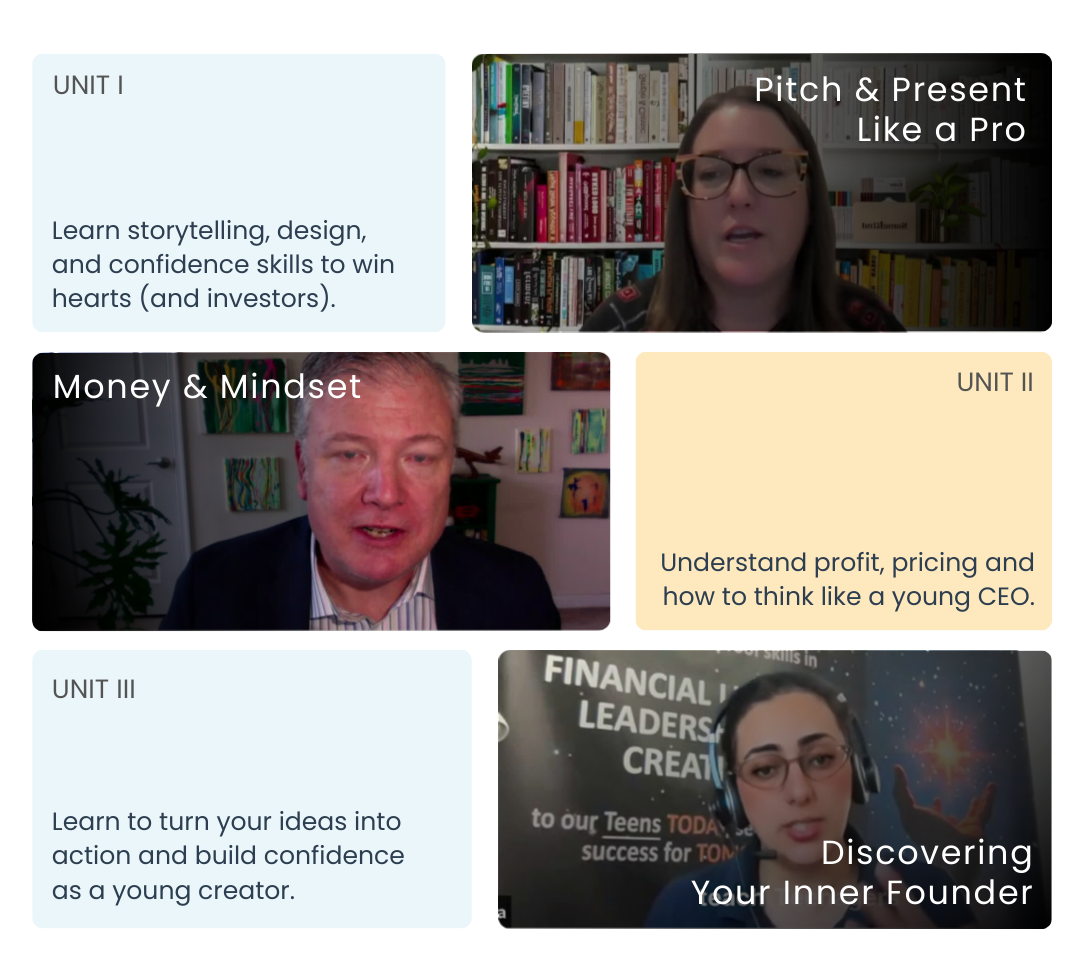

The Essentials of

Entrepreneurship

WHY SOT

Real-World Startup

Insights

Gain hands-on experience and actionable skills. SOT provides real-world tactics and frameworks, taught by experts.

WHY SOT

Learn On Your Own

Time

Flexible, self-paced education for entrepreneurs. Access the best alternative MBA—anywhere, anytime, on any device.

WHY SOT

Connect With Fellow

Founders

Get support from your peers through online webinars and in-person networking events.

Our Community

Student Testimonials

I have two daughters, a late teenager and one who is in her early twenties. Both have benefited tremendously from the SOT program.

Deanna G.

Parent

I learned techniques to ground myself and prepare for public speaking. The leadership module gave me real confidence.

Katherine E.

26, Recent Graduate

SOT's Gen Z MBA gave me practical leadership tools within the first 2 weeks. I use them daily in my business.

Sidney H.

24, Astrologer

I did the financial and the leadership that SOT offers. It was amazing. The real-world frameworks are invaluable.

Maya R.

IT

I thought leadership was a matter of confidence—something a person either had or didn't. SOT changed that for me.

Fikri S.

29, Medical Student

The AI cash-up turned a pile of receipts into a clean P&L in minutes. Game changer for my small business.

Jaxon R., 22

Finance intern (AI + Money)

The pricing game changed everything. Our AOV nudged from $9.50 to $10.60 — that's real money at scale.

Aria K.

19, Gap-year Builder

I thought I needed a co-founder. Turns out I needed an AI teammate. SOT showed me how to build one.

Leo M., 24

CS grad pivoting to product (AI ops + Leadership)

Stand out with the

Superstars of

Tomorrow Certificate

Earn a certificate upon completion and display your business credentials on your resume & Social Media

ENROLL NOW

Our Mission

Traditional MBA vs Gen Z MBA™

Traditional MBAs

- $100,000 tuition, on average

- Inflexible learning

- 2 year time commitment

- Outdated, rigid curriculum

- Tedious admission process

Our Gen Z MBA

- $4200, with payment plans

- Anywhere, anytime

- 30-minute / day

- Constantly updated curriculum

- Open education

7-Day Money-Back

Guarantee

Try Superstars of Tomorrow for 7 days & if you are not completely satisfied,

you can claim a full refund - no questions asked.

Frequently

Asked Questions

Yes! Our program is designed for ages 13–27, with a strong focus on young adults 18 and up. We have students from various backgrounds and experience levels. The curriculum adapts to meet each student where they are.

About 1 hour per week for live sessions, plus approximately 30 minutes of daily practice. The program is designed to fit around school and other activities.

All live sessions are recorded and available on-demand. You can watch at your convenience and still participate in the community discussions.

Absolutely. Students build a Portfolio Dossier with real business projects, leadership examples, and verified skills — exactly what admissions officers look for.

Yes. The skills taught — leadership, financial literacy, communication, AI — are valuable regardless of career path. Many students discover passions they didn't know they had.

We'd Love to Hear

From You

Whether you've got a question or feedback, drop us a message and we'll be in touch shortly!

SEND MESSAGE